Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Digital Nomad Budgeting is the difference between freedom and financial stress. Digital nomadism promises flexibility, new countries, and location-independent income, but without strong budgeting systems, that freedom can quickly become overwhelming. Currency fluctuations, irregular income, visa costs, and rising global living expenses make budgeting far more complex for nomads than for traditional workers.

According to global cost-of-living data from Numbeo, expenses can vary dramatically between cities, even within the same country. Successful digital nomads are not necessarily the highest earners; they are disciplined planners who understand where their money goes and how to control it.

This article outlines seven smart and proven budgeting plans that help digital nomads stay financially stable, avoid surprises, and build long-term sustainability while living and working anywhere in the world.

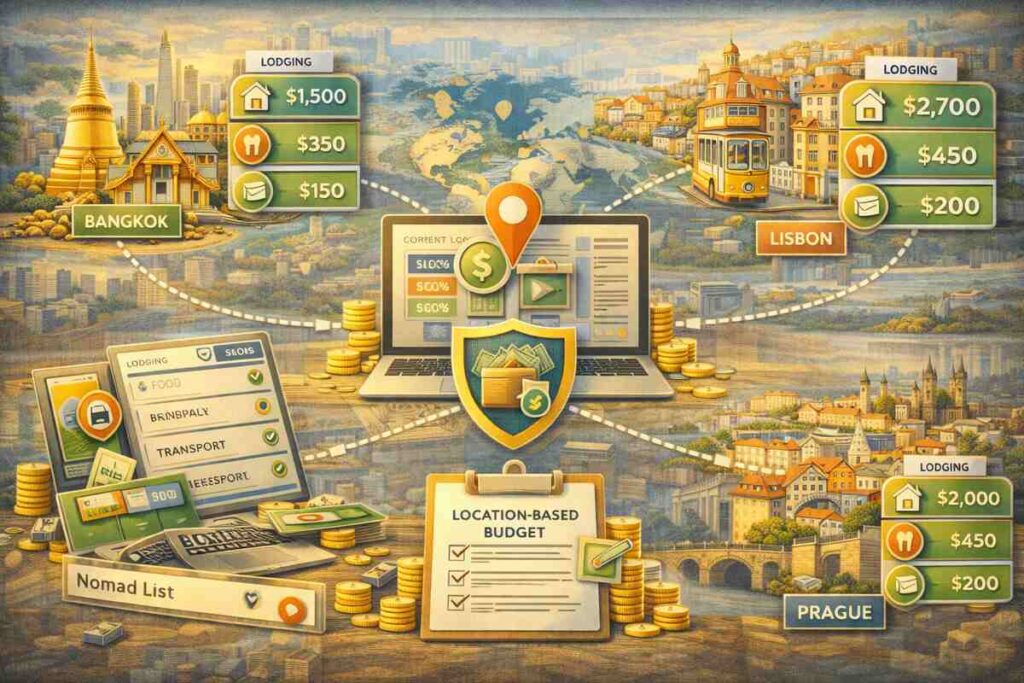

Traditional budgets assume stable rent, utilities, and transportation costs. Nomad life breaks that assumption.

Smart nomads create location-based budgets that adjust every time they move. Cost-of-living platforms like Nomad List provide real-world data on rent, food, coworking, and transportation in hundreds of cities.

How to apply this plan:

This approach prevents underestimating expenses in high-demand nomad hubs.

Blended finances are one of the fastest ways to lose control of your budget.

Financial advisors highlighted by Investopedia consistently recommend separating accounts to improve clarity and reduce tax errors.

Best practice setup:

Separation makes it easier to track spending, manage taxes, and identify leaks.

The classic 50/30/20 budgeting rule (needs, wants, savings) still works, but nomads must adapt it.

Remote workers often face variable income and fluctuating costs. Guidance from NerdWallet suggests adjusting percentages based on income stability.

Nomad-friendly version:

Flexibility is key. The goal is balance, not rigidity.

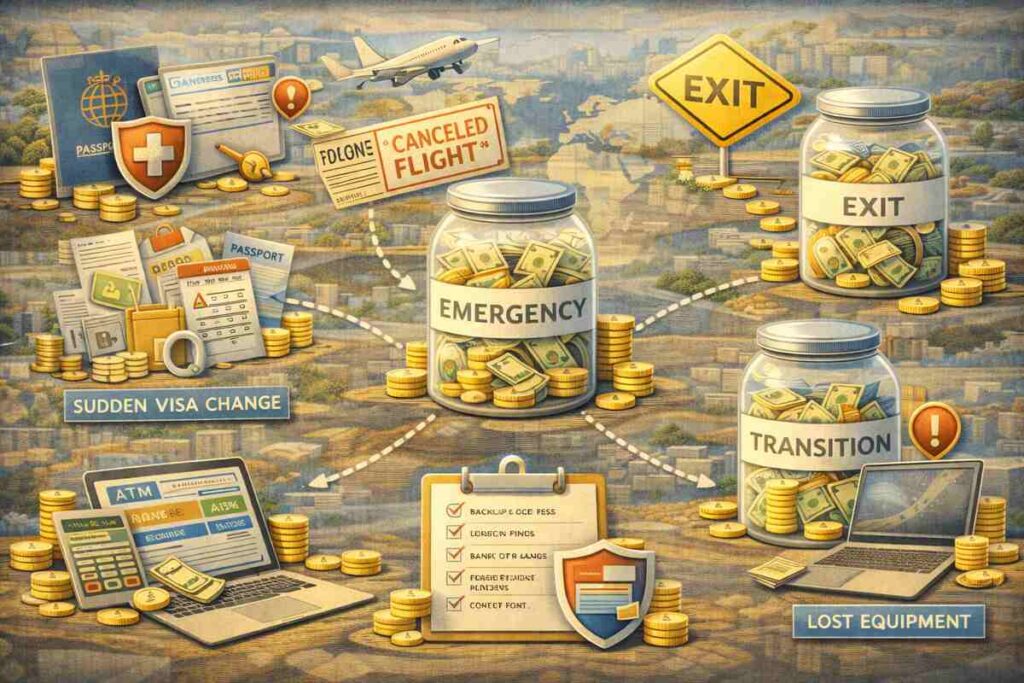

For digital nomads, emergencies include more than medical bills.

Sudden visa changes, flight cancellations, lost equipment, or political instability can force rapid relocation. Research from World Nomads highlights how unplanned disruptions affect long-term travelers.

What to prepare for:

Emergency planning protects both income and mobility.

Hidden fees quietly destroy nomad budgets.

ATM charges, poor exchange rates, and foreign transaction fees add up quickly. Reviews from Wise explain how multi-currency accounts reduce conversion losses.

Smart money strategies:

Reducing friction keeps more money in your pocket.

Nomad spending changes fast. Monthly reviews are often too late.

Behavioral finance insights from Harvard Business Review show that frequent tracking increases financial discipline and awareness.

Effective tracking habits:

Consistency matters more than perfection.

Many nomads budget only for the next destination, but forget the future.

Long-term financial planning includes retirement, healthcare, and income gaps. Guidance from Vanguard emphasizes early, consistent investing, even with irregular income.

Long-term considerations:

Sustainable nomadism requires thinking beyond the next flight.

Even experienced nomads overspend when they:

Avoiding these mistakes is as important as following budgeting plans.

Digital nomad budgeting is not about restriction, it’s about control. The seven plans outlined here provide structure without killing spontaneity.

By planning per location, separating finances, tracking expenses regularly, and preparing for emergencies, nomads can enjoy freedom without financial anxiety.

Smart budgeting doesn’t limit your journey, it sustains it.